Accelerating AI Computing to Fuel ADAS Evolution

AD/ADAS computing demands both a new speed of semiconductor development and performance. This has led to the rise of several startups to develop both SoCs and AI accelerators for AD/ADAS. USD $96.7B ADAS market opportunity by 2030, as projected by UBS, makes this even more attractive.

High-performance Computing is Essential

Changing lanes and heeding traffic lights. What millions do routinely during their commutes illustrates some of the critical bottlenecks in current AD/ADAS computing. Besides changing lanes, mere mortals can easily identify, analyze, and anticipate pedestrian intent, as well as determine the phases of a traffic light from a fairly long distance, day or night, and in real-time.

For an ADAS application to function successfully in an individual vehicle, it must first identify small objects that could be stationary or moving, and up to 250m away. Most modern vehicles already have multiple high-resolution cameras, up to 8MP to capture images. However, analyzing the volume of data acquired from multiple cameras and other sensors, and acting responsibly in real-time demand both exceptionally high-performance and low-latency computing with optimal power efficiency.

Scaling to many cars on a busy street, systems must also be able to work seamlessly in real-time with other vehicles and sensors in proximity, and at Big-Data-like volume that adheres to stringent privacy/security requirements. How must ADAS computing evolve to execute this at least as well as humans do today and at scale? The answer may lie in purpose-built, power-efficient SoCs developed not by traditional automotive manufacturers, but by a new set of agile startups.

AD/ADAS Compute Is Positioned for Growth

Computing is estimated to represent more than ten percent of the annual market opportunity for ADAS by 2025 (Source: Bank of America). This is driven by the ADAS market, which is estimated to be USD 96.7B by 2030, growing at over 30% CAGR (Source: UBS Global Research).

To change lanes or heed traffic lights, an inferencing system requires exceptional computational efficiency. For example, it must identify a euro standard pallet (20cm x 20cm x 40cm) from 160m distance in any lighting condition. Doing this successfully requires at least 8 MP camera resolution and a 120dB dynamic range image sensor operating at 40 fps. The processing power required to infer such classes of objects will require a few hundred TOPs while operating at 25ms cadence.

ADAS computing systems include both Systems on a Chip (SoCs) and specialized AI Accelerator Chips, to leverage deep neural network algorithms as efficiently as possible. Beyond optimizing performance per watt, or performance per SoC footprint, these new devices must also speed up Deep Learning for perception and sensor fusion tasks.

High-performance, low-latency ADAS computing depends on processing power delivered by these new types of SoCs. AI Accelerator SoCs will determine the overall system performance, and hence command a major share in profit margins of the ADCU system. The transition from decentralized to centralized architecture is further driving the growth of AD/ADAS compute.

Learning from Adjacent Industries—Smartphones

The smartphone industry shows that prioritizing compute to drive overall system performance is a successful long-term strategy. While the initial success of higher-end smartphones resulted from the combination of a fantastic user experience paired with robust SDKs to enable millions of developers to create an app ecosystem, its continued success, market leadership, and profitability are based on making compute a foundational strategy. Full control of compute and software architecture remains essential to build a strong, consistent OS layer and maintaining control over the system costs.

A virtuous cycle of key building blocks, which includes Compute Chips, was a major factor in Apple’s success. Apple insourced chip development (acquired PA Semi), which was previously sourced from Intel. The net result is that, though Apple has a market share of less than 20% of the smartphone sales, Apple still commands over 60% of the net profits.

(Source: Counterpoint Research, Dec 2019)

Prioritizing Compute: Automotive Parallels the Smartphone industry

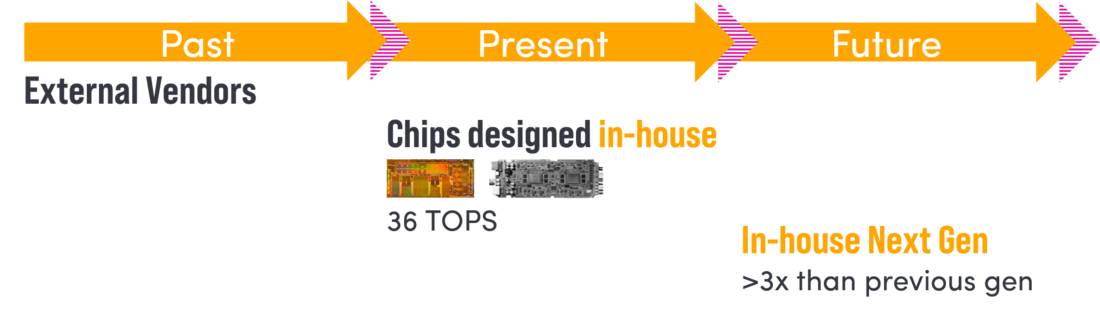

Tesla seems to have already taken the cue from the smartphone industry by prioritizing SoC development to increase computing power. After initially sourcing from Mobileye, Tesla insourced its AI SoC. While there may have been other contributing factors, insourced AI chips and control over SW-HW co-design have significantly contributed to Tesla’s AutoPilot development. While the current generation of these chips are ~36x2 TOPs, the next-generation chips are expected to be over 3x superior and will continue to raise the bar.

Given the increasing focus and Tesla’s 10x growth, it is a question of when (and not if) the rest of the Automotive manufacturers prioritize a similar AD/ADAS compute strategy. Compute is essential for ADAS due to the sheer volume of data that must be processed in-vehicle and in real-time. Success will come to those to take the early challenge head-on to maintain safety and market advantage.

(Source: Tesla Autonomy day; Electrek.co Tesla HW 4.0, Wiki FSD chip)

AI Semiconductor Landscape

Traditional automotive semiconductor manufacturers are lagging in their AI development as they must simultaneously contend with incremental near-term ADAS features for L2. This means opportunities for agile, innovative startups or spinouts to define and develop compute systems and chipsets for L3 and beyond.

Currently NVIDIA and Mobileye target this performance gap. Both leverage their leadership in GPUs and Smart Camera respectively. Combined with software toolchains and future roadmaps, both companies will raise the bar with subsequent releases.

Despite their promising roadmaps, there is still room for a giant leap in PPACAT (Performance Power Area Cost Accuracy Tools). This can only be accelerated by newer companies fostering healthy competition. At the end of the day, developing AI SoCs is a game of efficiency, safety, and yes, profitability.

It is a near-greenfield opportunity for start-ups and new entrants. In the last few years, over 45 startups have emerged in the specialized AI chip space, including non-automotive applications as well. Over $3B venture capital investments went into this sector in the last four years, comprising of over 20 startups. These include AIStorm, AlphaICs, Ambiq, Baecsense, Blaize, Cambricon (IPO), Cerebras Systems, DeepVision AI, EDGENeural AI, Efinix, Flex Logix Technologies, Graphcore, Groq, Hailo, Horizon Robotics, Kneron, Mythic, Nuvia(acquired), Recogni, SambaNova, SiMa.ai, Syntiant, Tenstrorrent, Untether AI, Vastai Tech, Wave Computing, Xceler Systems, etc. (source: Pitchbook, 2021).

Of these startups, Blaize, Hailo, Horizon Robotics, and Recogni are more focused on AD/ADAS applications. Horizon Robotics and Recogni stand out with their higher targets for performance and power efficiency.

AD/ADAS Computing is an Open Opportunity

Startups, “intrapreneurs” of traditional companies, and spinouts within the Compute, Data Center, and AI/ML accelerator SoCs segments are poised to re-define and develop the computing gap left by traditional automotive semiconductor vendors. AI accelerator SoCs can deliver high-performance, low-latency, power-efficient computing in ADAS applications, as well as high value for its automotive OEMs. These smaller, agile companies provide the innovative spark to move the industry collectively forward, and companies like Continental can assist by leveraging its scale and ecosystem partners.

Once proven, AI-enabled vehicles can give drivers and passengers peace of mind, an important emotional hurdle for transitioning to autonomous driving. Purpose-built, power-efficient SoCs and AI accelerators will reliably enable higher levels of ADAS and true autonomous driving, fostering safer, more efficient vehicles all over the world.

Key contributors

This article wouldn't have been possible without the help of my colleagues at co-pace and Continental AG (www.co-pace.com), Michael Rolfes, Chen Zhang and Juergen Bilo, and discussions with several thought leaders from the startup ecosystem. co-pace creates new product portfolios and onboard disruptive innovation through partnership with startups. To do this, we dive deep into the future tech. This post is the result of our team’s work and it offers a glimpse into our thinking. We’ve love to know what you think – reach out to us and let’s continue the conversation!